Tweet

Tweet

2 years for inquiries

-

-

Then they would be wrong..Originally posted by 2011GT View Post

I've had an 847 when I got the lease on the BMW and have only one unpaid credit card with only $200 charged to it. Then there is the car payments and mortgage. Doing things like paying your bill on time, maintaining a favorable income to debt ratio, keeping up a constant but small rotating debt amount (credit cards).

After getting the lease my score dropped to 792. I expect it to drop a little more when we finish buying the house next month but it'll come back up soon because we are about to pay off our Adoption loan. We aren't that far from paying off my wife's car.Comment

-

You are pathetic. needing all that debt. You should be ashamed.Originally posted by Sgt Beavis View Post

Seriously though. i thought it was a credit to debt ratio that mattered. Never heard of the income to debt ratio.Comment

-

I believe credit to debt matters as well but income to debt (money coming in against money going out) matters a lot.Originally posted by mstng86 View Post

Also, if I recall correctly, having too much revolving credit (even if it is unused) can hurt you because it is easy for you to go deep in debt very quickly..Comment

-

Originally posted by krazy kris View PostAll mortgage inquiries within 30 days of the first count as one according to the agency where we pull our reports. I would imagine the auto and revolving inquiries are similar. If you're seeing different scores it is probably because of the different models used by different creditors, not because your score actually went down.Originally posted by Big A View Post

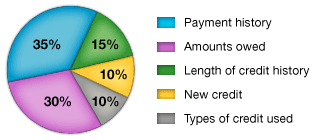

This graph shows what makes up the score (at least on the mortgage FICO model):

Comment

-

So, how much does checking your score hurt you?Comment

-

Ah, so maybe it didn't affect the score, they just both showed up as inquiries.Originally posted by SVT Lurch View Post

I don't think that it does, as long as you're using a reporting service. If you aren't, and are applying for cards, and then requesting after a denial, then yeah.Originally posted by 4EyedTurd View Post

Unless you are talking having it checked for a loan, then a creditor pulling your report shows as a hard inquiry, and you score will go down a little. It's not much if it's just 1 or 2, but the more you have at any given time affects it even more. When I moved to Sac, I already still had my car and a credit card inquiry. Then the leasing company pulled it, the cable company did, and PG&E (utilities), and I think it dropped like 40 points IIRC.Comment

-

Originally posted by Big A View Post

I was thinking about checking it since I've knocked out a good bit of debt recently. Anyone wanna recommend a reporting service?Comment

-

I use freecreditreport.com, I guess those stupid commercials actually do work. I wanna say that you can request a copy of your report once every so often, like every 6 months or a year, but I don't recall.Originally posted by 4EyedTurd View Post

FWIW paying off debt will help your credit to debt, and debt to income, but it didn't make mine move much back when I paid off my truck and all credit cards. I have some blemishes from back when I was out of work after my wreck though, and unable to pay some of the medical bills, so I am sure that outweighs the above quite a bit. I've been trying to get back on top ever since, to be able to get a decent rate on a new house, thus wanting to monitor my score.

Not to say I didn't owe the bills, it's just irks me knowing how much all involved made off of my insurance, and it still put me in a bind (physically and financially).Comment

-

I started using freecreditreport as well. Only because I am still trying to increase my credit score while just starting to get things in order for a new house. I want tonight an idea where I am at all times and make sure no fraud is taking place. I do know that a mortgage loan inquiry took it down about 15 points. I have gained about 40 points in the last 6 months after paying off cc debt.Originally posted by Big A View PostComment

-

Sub-700s were fine 5 years ago. I'm generalizing here, but 720-740 is the new 650 - however, I'm surprised you still got straight denied at 685. I would've thought you'd at least be offered a loan at a higher interest rate.Originally posted by bonnie&clyde View Post

Also, the last I played in this was for my home mortgage. There was 50 point variations from one place to another. WTF?

I laughed at the higher your score the higher your debt. 1. It's all relative to income and 2. We all know plenty of people in the 800+ club with little to now debt. Or assets to cover if there were an issue.Originally posted by MR EDDComment

-

I've subscribed to myfico.com a few years ago and never stopped. You get a few free reports per year, constant monitor of your credit score with alerts and some analysis stuff.Originally posted by 4EyedTurd View Post

I really like the alerts, you get a pulse on anything you do that affects your score. Sometimes it's just the OPPOSITE of what you think will happen, but you know within a week.

It's a 100 bucks or so for a year service, but you can usually find coupon codes that make it 50-75 dollars.Originally posted by MR EDDComment

-

-

annualcreditreport.com is where you get your free credit report pulls once a year. I subscribe to the creditcheck service through USAA for $13 a month that allows unlimited pulls from all three agencies and gives you approximate scores.Comment

Comment